Use of s. 88(1)(d) in buy, bump and sell transactions (p. 937)

The introduction of the foreign affiliate dumping (FAD) rules in 2012 makes the 88(1)(d) bump more important than ever to foreign purchasers. The FAD rules create significant adverse (and ongoing) Canadian tax consequences for foreign-controlled Canadian corporations with foreign subsidiaries, and they effectively encourage Canadian group members to dispose of existing foreign affiliates whenever possible. Amendments made to the version of the FAD rules enacted in late 2012 facilitate the use of the 88(1)(d) bump in these circumstances, and when the 88(1)(d) bump is available to reduce or eliminate Canadian CGT [capital gains tax] on shares of foreign affiliates (and there are no tax impediments in the foreign affiliate's home country), it will generally be the primary tool used by foreign purchasers of a Canadian corporation that owns foreign subsidiaries to avoid having to contend with the FAD rules on an ongoing basis.

Purpose of anti-stuffing rule in s

88(1)(c)(v) (p. 942)

Another rule is meant to prevent the parent from transferring property with accrued gains to a subsidiary on a tax-deferred basis before the AOC and eliminating those gains on the wind-up through the 88(1)(d) bump. This ''anti-stuffing'' rule disqualifies any property that the subsidiary acquires (as part of the AOC [acquisition of control] series) from either the parent or a person dealing NAL [not at arm's length] with the parent. That property, as well as any property acquired by the subsidiary in substitution for such property (an issue discussed below), is excluded from being eligible property.

Policy of bump denial rules (p. 946)

The policy behind the bump denial rule is deceptively simple: The parent should not be able to buy and wind up the subsidiary, claim an 88(1)(d) bump on its property, and then sell some of that property back to the subsidiary's former shareholders….

Prohibited persons/prohibited property (p. 947)

…At a core level:

- prohibited persons are shareholders of the subsidiary at a time that is both before the AOC and during the AOC series; and

- prohibited property is property distributed to the parent on the wind-up (that is, acquired from the subsidiary when it is merged or wound up into the parent).

The basic thrust of the bump denial rule is that property of the subsidiary that is distributed to the parent on the wind-up (herein, distributed property) should not, as part of the AOC series, be acquired by persons who were significant subsidiary shareholders at a time during the AOC series and before the parent acquired control of the subsidiary. The term ''significant'' for this purpose essentially means holding 10 percent or more of a class of the subsidiary's shares, individually or collectively.

Examples of prohibited persons (pp. 947-8)

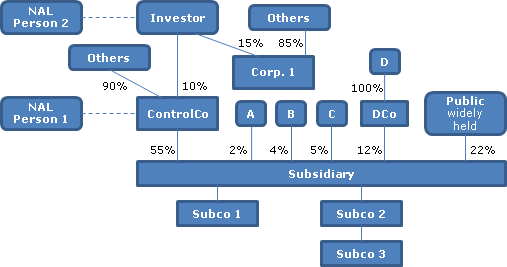

The most useful way to illustrate the wide range of potential prohibited persons is by using the example shown in Figure 6, as annotated by the discussion in the text accompanying footnotes 42-47 and 51.

1. Persons Owning (or Deemed to Own) 10-Plus Percent of a Relevant Class of Shares Pre-AOC [acquisition of control]

. The prohibited persons concept centers on persons who are specified shareholders of the subsidiary at a time that is both before the AOC and during the AOC series (herein, a pre-AOC subsidiary specified shareholder)….

- Ownership of Shares in Related Upstream Corporations: a person is deemed to be a specified shareholder of a particular corporation if that person meets the 10 percent share ownership (or deemed share ownership) threshold in any other corporation that both:

- is related to the first corporation; and

- has a ''significant direct or indirect interest'' in the first corporation — that is, an ''upstream'' related corporation. [fn 44: …Investor owns 10 percent of the shares of a corporation (ControlCo) that:

- is related to the subsidiary (since ControlCo has legal control of the subsidiary); and

- has a significant direct or indirect interest in the subsidiary. NAL [non-arm's length] Person 2 (who deals at NAL with Investor) is deemed to own Investor's shares of ControlCo, and is thus in the same position as Investor.]

2. Other Prohibited Persons

The prohibited person definition goes beyond pre-AOC subsidiary specified shareholders to include the following persons:

(a) any number of persons whose collective share ownership, if aggregated in the hands of one person, would make that one person a pre-AOC subsidiary specified shareholder [fn 45: For example, see A, B, and C collectively in Figure 6 since their shareholdings would, if aggregated, make the holder a specified shareholder of the subsidiary by virtue of owning more than 10 percent of its shares. If A, B, and C all acquired any prohibited property as part of the AOC series, the bump denial rule would apply.]

(b) a corporation, other than the subsidiary, in which a pre-AOC subsidiary specified shareholder is, at any time after the AOC and during the AOC series, a specified shareholder [fn 46: See, e.g., Corp. 1 in Figure 6, which is a corporation more than 10 percent of the shares of which are owned by a pre-AOC subsidiary specified shareholder (Investor) following the AOC.]; or

(c) a corporation, other than the subsidiary, if:

- persons described in (a) above acquired shares as part of the AOC series; and

- those acquired shares would, if aggregated in the hands of one person, make that single notional person a specified shareholder of that corporation at any time after the AOC and during the AOC series. [fn 47: For example, any corporation of which A, B, and C collectively own 10 percent or more of the shares of any class, if they acquired those shares as part of the AOC series.]

Again, in all cases, the parent and anyone dealing at NAL with the parent will not be a prohibited person.

10%-plus properties as prohibited property (p. 951)

2. Property Deriving More Than 10 Percent of Its FMV From Distributed Property Post-AOC [acquisition of control]. Typically, the main concern with the scope of prohibited property is property that derives more than 10 percent of its FMV from distributed property at a time following the AOC and when owned by the prohibited person (herein, 10 percent-plus property). One of the most common examples of 10 percent-plus property is shares of an acquirer of the subsidiary (or of that acquirer's own controlling shareholder)….

Exclusions in s. 88(1)(c.3)

Some properties specified in the ITA that are 10 percent-plus property are excluded from being deemed substituted property. …

These are important exceptions, since they allow, for example, the parent to issue shares or debt in exchange for money in order to finance an acquisition of the subsidiary, without having to worry about whether the persons acquiring the shares or debt are prohibited persons. They also allow a taxable Canadian corporation to issue shares of itself directly in exchange for shares of the subsidiary, which permits Canadian acquirers to use their shares as currency to acquire the subsidiary without creating prohibited property. [fn 57: Moreover, since for these purposes a ''share'' includes a right to acquire a share (paragraph 88(1)(c.9) of the ITA), employee stock options to acquire subsidiary shares can be exchanged for employee stock options to acquire parent shares. Note, however, that this exception does not extend to stock options issued for other consideration — for example, options issued to subsidiary employees as an incentive to remain with the company post-AOC [acquisition of control].]

Exceptions do not extend to foreign securities (p. 953)

Unfortunately, none of these exceptions apply to shares or debt issued by non-Canadian corporations (other than the exception for debt issued solely for money). As such, securities of a foreign entity that is the direct or indirect acquirer of the subsidiary will generally constitute deemed substituted property, unless either:

- the securities are debt issued in exchange for money; or

- the foreign entity is so much larger than the Canadian target subsidiary that the foreign entity's securities cannot be said to derive more than 10 percent of their value from the Canadian target subsidiary's assets (that is, distributed property).

The result is that Canadian acquirers have an advantage over foreign acquirers in that they can use their shares and debt to pay for the shares of Canadian targets and still be able to claim the 88(1)(d) bump. If Canadian target shareholders who collectively hold 10 percent or more of the Canadian target's shares receive shares or debt of a foreign acquirer for their Canadian target shares, and if those foreign acquirer shares or debt derive more than 10 percent of their value from the Canadian target's properties, persons who in aggregate constitute a pre-AOC subsidiary specified shareholder will have received prohibited property, and the bump denial rule will apply. Hence, a foreign acquirer can generally use the 88(1)(d) bump only if it pays cash or if it acquires a Canadian corporation representing less than 10 percent of the acquirer's own value.

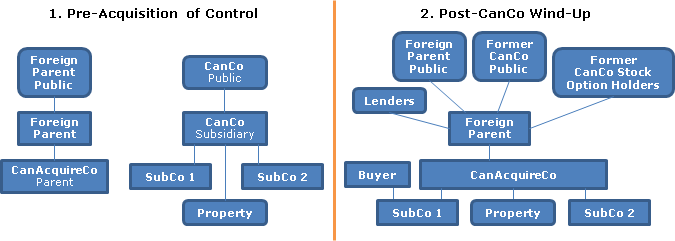

Example of problems arising on foreign acquisition (pp. 953-4)

Figure 9 illustrates some of the typical problems that can arise when a foreign acquirer (Foreign Parent) acquires a public Canadian target (CanCo) in exchange for Foreign Parent shares, using a Canadian corporation (CanAcquireCo):

- Foreign Parent shares would be prohibited property if more than 10 percent of their post-AOC FMV is attributable to CanCo's property. [fn 63: In ''exchangeable share'' transactions, CanCo shareholders receive exchangeable shares of CanAcquireCo that track the value of, and will ultimately be exchanged for, Foreign Parent shares. In such circumstances, while CanAcquireCo exchangeable shares may be ''specified property'' and thereby excepted from being prohibited property, the ultimate exchange of exchangeable shares for Foreign Parent shares would generally trigger the application of the bump denial rule if those Foreign Parent shares are 10 percent-plus property so as to be prohibited property….]

- Holders of CanCo employee stock options who exchange their options for Foreign Parent stock options will have acquired deemed substituted property (and thus prohibited property) if more than 10 percent of the options' post-AOC FMV is attributable to CanCo's property.

- A Foreign Parent receivable acquired by a lender as part of the AOC series would be a prohibited property if more than 10 percent of its post-AOC FMV is attributable to CanCo's property, unless it was issued solely for money.

- If after the wind-up, Foreign Parent disposes of SubCo 1 (a distributed property) to Buyer, it is important that Buyer not be a prohibited person. Buyer's own securities will also become prohibited property if they derive more than 10 percent of their FMV from the SubCo 1 shares (which are distributed property), creating the need to determine if Buyer's shareholders include former CanCo shareholders (prohibited persons). [fn 64: If Buyer securities are acquired as part of the AOC series by a single pre-AOC CanCo specified shareholder (a prohibited person) or by a number of smaller pre-AOC CanCo shareholders whose collective shareholdings would make a single holder of them a pre-AOC CanCo specified shareholder, the 88(1)(d) bump will be tainted. As described in Section VII.A.2, Buyer will itself be a prohibited person (tainting the bump if the purchase of SubCo 1 is part of the AOC series) if either:

- a single pre-AOC CanCo specified shareholder is also a post-AOC specified shareholder of Buyer (regardless of whether that shareholder acquired its Buyer shares as part of the AOC series); or

- as part of the AOC series, a number of smaller pre-AOC CanCo shareholders whose collective shareholdings would make a single holder of them a pre-AOC CanCo specified shareholder acquire enough Buyer securities to make a single holder of them a specified shareholder of Buyer following the AOC.] This is an important issue since one of the primary uses of the 88(1)(d) bump is on the post-wind-up sale of distributed property to third parties.

Changes to directly-held properties before acquisition of control ("AOC") (p. 941)

The requirement [in the midamble of s. 88(1)(c)] that eligible property be owned directly by the subsidiary at the time of the AOC means that the subsidiary can influence whether an 88(1)(d) bump will be available to the parent following the AOC and which properties would be eligible properties. Before the AOC, the subsidiary can change which properties it owns directly, sell or acquire properties, or take other steps to affect the parent's ability to claim an 88(1)(d) bump. It is often in the parent's interests to conclude an agreement with the subsidiary (or its shareholders) before the AOC to prevent the subsidiary from taking any actions that would impair the 88(1)(d) bump, or to require the subsidiary to take reasonable actions to enhance the 88(1)(d) bump. This form of agreement can add significant value to the parent.

Summary of s. 88(1)(d)(ii.1)

… Expressed conceptually, the FMV of the partnership interest is deemed to be reduced by an amount representing that portion of the subsidiary's accrued gain on the partnership interest that is attributable to the sum of:

- the FMV of Canadian or foreign resource property owned by the partnership (directly or through other partnerships); and

- the difference between the FMV and cost amount of other forms of non-eligible property (for example, depreciable property or inventory) owned by the partnership, either directly or through other partnerships. [fn 29: The Department of Finance explanatory notes accompanying the relevant provisions of the ITA make clear that this rule does not reduce the amount of an 88(1)(d) bump regarding an interest in a partnership that owns shares of a corporation simply because the corporation owns non-eligible property.]

Example: bump reduction for ineligible appreciation (p. 944)

For example, consider the case of a partnership interest held by the subsidiary at a tax cost of $70 and whose FMV is $100 (that is, a $30 accrued gain). If the partnership itself owns an eligible property with a tax cost of $5 and an FMV of $10, and a non-eligible property with a cost amount of $65 and an FMV of $90, for purposes of the general limitation in Section VI.A.1 above, the FMV of the partnership interest would be deemed to be $75 instead of $100. [fn 30: The reduction in the FMV of the partnership interest is computed as the portion of the accrued gain on that property that is attributable to the notional gains on non-eligible property. Since the notional gains on the non-eligible property represent five-sixths ($25 / ($5 + $25)) of the total accrued gain ($30), for this purpose the FMV of the partnership interest ($100) is reduced by $25 (five-sixths of the $30 accrued gain on the partnership interest)] This means that the maximum s. 88(1)(d) bump on such partnership interest would be $5 ($75-$70).

Buy, bump and sell transactions of foreign acquirer (p. 937)

The introduction of the foreign affiliate dumping (FAD) rules in 2012 makes the 88(1)(d) bump more important than ever to foreign purchasers. The FAD rules create significant adverse (and ongoing) Canadian tax consequences for foreign-controlled Canadian corporations with foreign subsidiaries, and they effectively encourage Canadian group members to dispose of existing foreign affiliates whenever possible. Amendments made to the version of the FAD rules enacted in late 2012 facilitate the use of the 88(1)(d) bump in these circumstances, and when the 88(1)(d) bump is available to reduce or eliminate Canadian CGT [capital gains tax] on shares of foreign affiliates (and there are no tax impediments in the foreign affiliate's home country), it will generally be the primary tool used by foreign purchasers of a Canadian corporation that owns foreign subsidiaries to avoid having to contend with the FAD rules on an ongoing basis.

General summary of surplus carve-out rule (p. 945)

…When control is acquired of a Canadian corporation that owns shares of a foreign affiliate, Canadian tax authorities perceive it as being duplicative to allow (in very general terms) the sum of the tax cost of the Canadian corporation's shares of the foreign affiliate and the amount of this ''good'' surplus the Canadian corporation has in the foreign affiliate to exceed the FMV of the Canadian corporation's shares of the foreign affiliate.

Accordingly, when the subsidiary owns shares of a foreign affiliate, an 88(1)(d) bump is not permitted to result in the sum of (1) the parent's tax cost of those shares and (2) the good surplus of the foreign affiliate at the time of the AOC [acquisition of control] exceeding the FMV of those shares. A comparable rule applies when the subsidiary owns shares of a foreign affiliate through a partnership….

General summary of bump limitation rule (p. 945)

…When control is acquired of a Canadian corporation that owns shares of a foreign affiliate, Canadian tax authorities perceive it as being duplicative to allow (in very general terms) the sum of the tax cost of the Canadian corporation's shares of the foreign affiliate and the amount of this ''good'' surplus the Canadian corporation has in the foreign affiliate to exceed the FMV of the Canadian corporation's shares of the foreign affiliate.

Accordingly, when the subsidiary owns shares of a foreign affiliate, an 88(1)(d) bump is not permitted to result in the sum of (1) the parent's tax cost of those shares and (2) the good surplus of the foreign affiliate at the time of the AOC exceeding the FMV of those shares. A comparable rule applies when the subsidiary owns shares of a foreign affiliate through a partnership….