BCE/GLENTEL -- summary under Shares for Shares or Cash

Overview

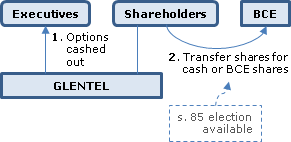

BCE will acquire GLENTEL under a CBCA Plan of Arrangement for cash or shares, at the GLENTEL shareholder's option, but with the overall consideration fixed at $295.4 million cash and BCE shares equal to 0.4974 of a BCE common share multiplied by 50% of the outstanding GLENTEL common shares. Both a s. 85.1 rollover (for those receiving only shares) and a s. 85 rollover (for those receiving a mixture) is available.

GLENTEL

A provider of wireless communication services listed on the TSX. Thomas Skidmore (the CEO) and A Allan Skidmore (Vice Chairman) hold 21.2% and 15.6% of the common shares.

BCE

Canada's largest communications company listed on the TSX and NYSE.

Plan of Arrangement

- Each outstanding option will be deemed to have been vested, with those with a lower exercise price than the "Cash Consideration" described below cash surrendered, and the others cancelled.

- Each common share of GLENTEL (other than those held by dissenting shareholders) will be transferred to BCE in consideration for the "Cash Consideration" (of $26.50 per share) or the "Share Consideration" (of 0.4974 of a BCE common share) at the shareholder's option subject to pro-ration based on the aggregate Cash Consideration and Share Consideration being fixed as described above - and with those not electing deemed to have elected the less popular option.

- Dissenting shareholders will be deemed to have transferred their GLENTEL shares to BCE.

Canadian tax consequences

A holder who receives only BCE common shares (other than cash in lieu of a fractional share) may defer gain under s. 85.1(1). A holder (including a non-resident holder) who receives both cash and BCE shares will be provided with a signed election form under s. 85(1) (or under s. 85(2) in the case of a partnership), provided the necessary information is provided to BCE within 90 days of the effective date of the Plan of Arrangement. In addition to posting a "Tax Instruction Letter" on its website, BCE will provide the letter to a duly requesting shareholder by email.

U.S. tax consequences

"BCE and GLENTEL do not plan to structure the Arrangement with the intended goal of satisfying [the] requirements" for "tax-free status" and "intend to take the position that the Arrangement is a taxable transaction."