Subsection 122.1(1) - Definitions

Gross REIT Revenue

Administrative Policy

22 February 2021 External T.I. 2018-0784661E5 - Subsection 122.1(1) - Gross REIT revenue tests

A mutual fund trust is the limited partner in a subsidiary partnership which is undertaking the development and construction of a new multi-unit...

23 December 2014 External T.I. 2014-0551841E5 - Subsections 44(1) and 69(11) of the Act

S. 69(11) can apply to deem a taxpayer which thought it disposed of property on a rollover basis to have received higher proceeds of disposition...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 44 - Subsection 44(1) | implied receipt of deemed s. 69(11) proceeds | 125 |

Investment

Articles

Shane Onufrechuk, Warren Pashkowick, "Tax Considerations of Major Construction Projects", 2014 Conference Report, Canadian Tax Foundation, 10:1-35.

Application of "replicate" test to public company investors (pp. 10:23-4)

[T]he "replicate test" within the definition of "investment" in...

Paragraph (a)

Subparagraph (a)ii)

Administrative Policy

2024 Ruling 2023-0997921R3 - Code 3 - XXXXXXXXXX SIFT Ruling Request

Background

The REIT, an open-ended unit trust and a REIT for ITA purposes, holds a Canadian real estate portfolio through subsidiary trusts and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 197 - Subsection 197(1) - SIFT Partnership | non-application of SIFT tax to REIT’s subsidiary LP issuing exchangeable units to tax-exempt | 328 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(7.1) | same proportionate taxable income allocation on sub LP exchangeable units avoided circumvention of s. 104(7.1) | 121 |

Non-portfolio Property

Administrative Policy

16 April 2015 External T.I. 2014-0561061E5 - Specified Foreign Property

The definition of "specified foreign property" in s. 233.3 excludes in para. (j) thereof a partnership interest where the property of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 233.3 - Subsection 233.3(1) - Specified Foreign Property | digital currency holdings of a foreign partnership not used in active business (para. (j)) | 180 |

Articles

Carrie A. Bereti, Edward Rowe, "Cross-Border Income Trusts", International Tax, No. 61, December 2011, p. 1

Includes description of North American Oil Trust structure (MFT on Canadian sub on US CFA).

Real Estate Investment Trust

Administrative Policy

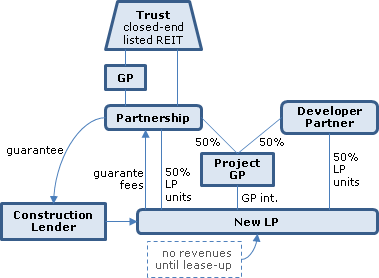

2014 Ruling 2014-0547491R3 - REIT entering into new LP

{kind=link}

Current structure

The Trust, a closed-end listed mutual fund trust which is intended to qualify as a REIT and indirectly owns retail, commercial...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 122.1 - Subsection 122.1(1) - Security | call and put rights not securities | 160 |

1 November 2010 External T.I. 2010-0368211E5 - Revenues of a REIT

Where a subtrust has allocated to a trust a taxable capital gain of $50 under s. 104(21), the trust will be considered to have derived a capital...

29 October 2010 External T.I. 2007-0244171E5 - SIFT Trust SIFT Partnership

Where a trust was a limited partner, its share of the revenues of the partnership would be revenues of the trust for purposes of paragraphs (b)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 122.1 - Subsection 122.1(1) - Rent from Real or Immovable Properties | qualifying non-participating rent under hotel lease | 90 |

Paragraph (a)

Administrative Policy

13 January 2022 External T.I. 2020-0845011E5 - Real estate investment trust - subsection 122.1(1)

A REIT holds units of a Canadian limited partnership which, in turn, holds inter alia all the shares of a U.S. subsidiary, which does not hold any...

Real or Immovable Property

Paragraph (b)

Administrative Policy

2011 Ruling 2010-0376801R3 - FIT Program (solar): revenue,

A REIT carries on its activities through a subsidiary LP. LP will participate in the Feed-in Tariff Program offered by the Ontario Power Authority...

Rent from Real or Immovable Properties

Administrative Policy

29 July 2019 External T.I. 2018-0784701E5 - Rent from real/immovable properties - furnishings

A mutual fund trust (the “Trust”) holds a limited partner interest in a limited partnership (the “Partnership”) which, in turn, holds...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) - Paragraph 132(6)(b) - Subparagraph 132(6)(b)(ii) | renting furnished apartments gave rise to rents | 30 |

29 October 2010 External T.I. 2007-0244171E5 - SIFT Trust SIFT Partnership

A net lease of a hotel or retirement residence by a trust to an arm's length operator thereof generally would qualify as giving rise to qualifying...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 122.1 - Subsection 122.1(1) - Real Estate Investment Trust | allocation of partnership revenue | 82 |

Security

Administrative Policy

2014 Ruling 2014-0547491R3 - REIT entering into new LP

Partnership, which effectively is wholly-owned by a REIT (the ‘Trust,") and "Developer Partner" (a partnership of corporations unaffiliated with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 122.1 - Subsection 122.1(1) - Real Estate Investment Trust | nil revenue satisfies the revenue tests/ provision of guarantee for fee not a business | 523 |

Subsection 122.1(1.2) - Character preservation rule

Administrative Policy

29 July 2011 External T.I. 2011-038551

All the units of Sub-trust 2 are held by Sub-trust 1 all of whose units, in turn, are held by a listed mutual fund trust. Rental income earned...

Subsection 122.1(2)

Administrative Policy

11 July 2008 External T.I. 2008-0267791E5 - normal growth guidelines -exchangeable units

Convertible or exchangeable securities issued by a lower-tier SIFT will be treated as an equity substitute which counts against the growth room of...